stock here: Anything the Josh Government does is apt to be suspect. Check the spreadsheet of ownership of land under the lake, and ownership of the spillway section. They have a new labryinth spillway design that at first glance will DO NOTHING in a major storm.

Ownerships:

Lake Wilson / Wahiawā Irrigation System

Ownership, Liability, and Tax Exposure Memo

Prepared from public State materials and parcel-level public listings

March 26, 2026

| Executive take: the public record does not show a simple one-owner Lake Wilson structure. Instead it points to a split system in which Dole-related entities, Wahiawā Water Company, and Sustainable Hawaii appear across different parcels and roles, while the State has been trying to assemble the whole package through Act 218. That fragmentation is the main reason the situation feels opaque—control, liability, and tax treatment do not sit neatly in one place. |

1. What appears to be happening

- The State’s own 2023–2026 materials treat the dam, spillway, reservoir, ditch system, outlet works, and related lands as an acquisition package rather than as a single obvious parcel.

- The named private-side owner pool in the State materials is Wahiawā Water Company, Inc.; Dole Food Company, Inc.; Sustainable Hawaii, LLC; or another appropriate owner.

- That strongly suggests the State itself has had to negotiate across a layered ownership map rather than a clean one-entity transfer.

2. Who appears to benefit

- Private holders retained fee interests in multiple parcels while the public carried the pressure to keep the flood-control and irrigation function alive.

- If a fragmented structure lets operations continue while delaying a full transfer, the private side can preserve bargaining leverage over price, remediation timing, easements, and transfer conditions.

- For agricultural users, the practical beneficiary of a State takeover would be system reliability; for the existing private-side owners, the practical benefit of delay is negotiating leverage.

3. Who appears to carry liability

- Historically, Dole Food Company Hawaiʻi was the entity publicly associated with the Wahiawā Dam remediation schedule.

- Act 218 and follow-on Board materials contemplate moving the reservoir-side parcels to DLNR and the broader irrigation-system parcels to ADC, which would shift future public responsibility onto the State.

- In practical terms, the pre-transfer picture appears to separate fee ownership, operational control, and dam-safety exposure.

4. Tax picture

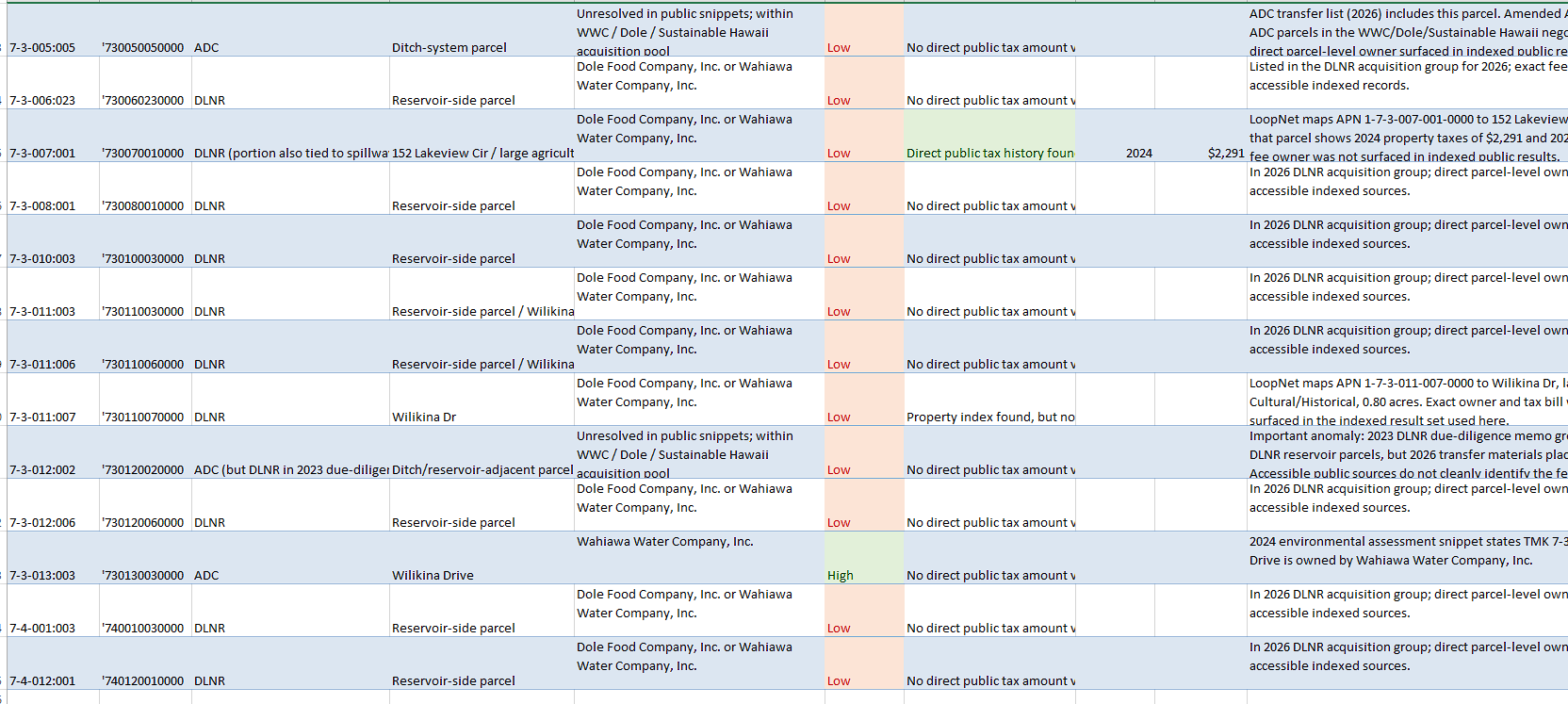

- At least some of the private parcels in the acquisition footprint were still showing regular Honolulu property-tax histories in public listings.

- Examples confirmed during the second pass: 71-129 Wilikina Dr (TMK 7-1-012:004) and 152 Lakeview Cir (TMK 7-3-007:001).

- That means the package was not purely a tax-exempt public holding before transfer; at least part of it was being treated as taxable private real property.

5. Why it feels ‘fishy’ – but what can and cannot be said

- Reasonable concern: the structure is hard for the public to understand because parcel ownership, operating responsibility, and safety responsibility are spread across multiple entities and agencies.

- Reasonable concern: some public documents describe the parcel groups differently over time, which makes the footprint look unstable or at least administratively messy.

- What cannot be fairly claimed from the current public record alone: that the fragmentation itself proves fraud, corruption, or an improper relationship. The stronger claim is opacity and complexity, not proven misconduct.

6. Cleanest bottom-line statement

The strongest defensible summary is this: Lake Wilson / the Wahiawā Irrigation System appears to have been held in a fragmented private structure involving at least Wahiawā Water Company, Dole, and Sustainable Hawaii, while the State has been trying to consolidate the dam, reservoir, and ditch system into public ownership. That fragmentation creates exactly the kind of blurred accountability that makes the arrangement look suspicious to outside observers.

7. Best next proof points if you want to push harder

- Pull the Bureau of Conveyances documents for each TMK and identify the current grantor/grantee chain.

- Match each TMK to Honolulu real-property tax records and note whether tax class, assessed owner, or exemptions changed just before transfer.

- Compare the parcel sets listed in 2023 due-diligence materials against the 2026 transfer package and flag additions, removals, and role changes.

Note: This memo separates verified public-record findings from inference. Where the record is incomplete, the wording is deliberately cautious.